Table of Contents

The $1.51 Trillion Semiconductor Squeeze: Why Your BOM Just Got More Expensive

I’ve been tracking semiconductor pricing for years, and I’ve never seen a setup quite like June 2026.

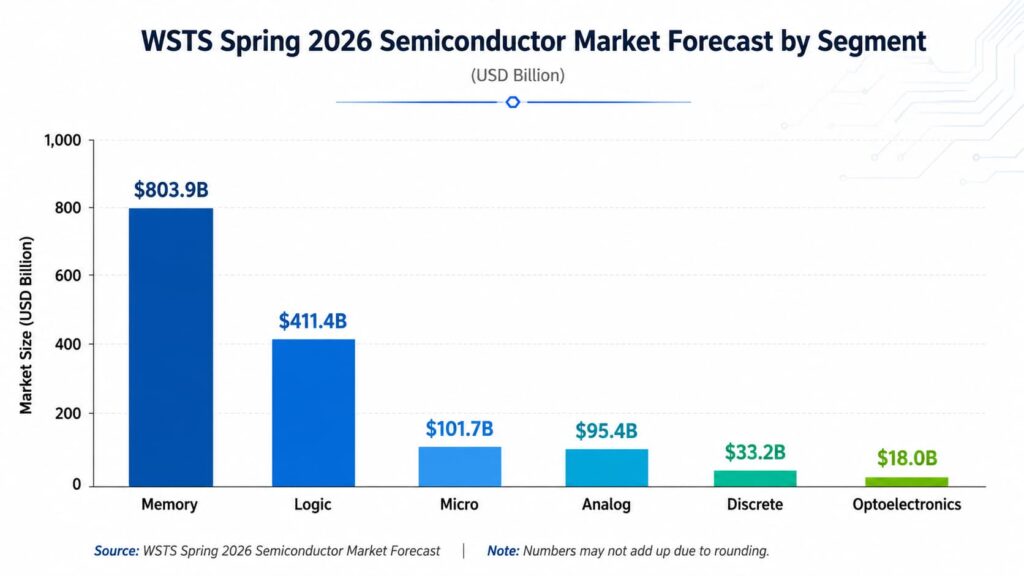

The market is projected to hit $1.51 trillion this year. That’s an 89.9% jump — WSTS‘s Spring forecast, not some blog’s hot take. Memory alone is up 249.5%. April chip sales cracked $110.5 billion, which is nearly double what they were a year ago.

And here’s the part that should bother you if you’re managing a BOM: TI just announced price hike number three. In one year. STMicro’s second round lands in six days. Infineon and NXP are already deep into multi-round territory. Goldman Sachs is calling it — DRAM contract prices at +300% year-over-year, the steepest memory inflation they’ve ever tracked.

So here we are. The biggest market in semiconductor history, and the tightest procurement environment most of us have ever worked through. Both things are true at once. That’s not a contradiction — it’s the definition of a structural squeeze.

1. The Numbers — and What They Actually Mean for You

WSTS broke it down in their Spring 2026 forecast. Here it is:

| Segment | 2025 Actual | 2026 Forecast | YoY Change |

|---|---|---|---|

| Total Semiconductor | $795.6B | $1.51T | +89.9% |

| Memory | $230B | $803.9B | +249.5% |

| Logic | $299.5B | $411.4B | +37.3% |

| Analog | $86.5B | $95.4B | +10.2% |

| Micro | $84.9B | $101.7B | +19.8% |

| Discrete | $30.7B | $33.2B | +8.0% |

Source: WSTS Spring 2026 Forecast (May 2026)

Let me point out the number that made me stop scrolling.

Memory now accounts for 53% of the global semiconductor market. A year ago it was 29%. When a single category nearly doubles its share of a $1.5 trillion market in twelve months, you’re not looking at a cycle. You’re looking at a power shift.

I’ll be honest — when WSTS first started revising their forecast upward last year, a lot of people (including me) wondered if they were overcorrecting. They weren’t. If anything, the revisions kept lagging reality. Goldman Sachs now puts the supply-demand gap at its worst in 15 years: DRAM deficit of 5.0% in 2026, widening to 5.9% in 2027. NAND at 4.4%. HBM at 5.1%. And their latest report says 2027 will be tighter than 2026, with the squeeze running into 2028.

Why? Because HBM — the high-bandwidth memory that AI accelerators guzzle — consumes 3 to 4 times more wafer capacity than conventional DRAM. SK hynix, Samsung, and Micron have sold out their entire 2026 HBM production. Every wafer that becomes HBM is a wafer that does not become DDR5, DDR4, or LPDDR. That’s the memory your industrial controller, your car’s ECU, and your laptop all need.

SIA‘s April numbers confirm this isn’t a blip: $110.5 billion in monthly sales, up 93.9% year-over-year. Q1 totaled $298.5 billion — a 25% jump from Q4. That’s acceleration, not cooling.

And Gartner? Their words: “meaningful price relief is unlikely before late 2027.” Phison CEO K.S. Pua has warned the memory shortage could persist for a decade. A decade. If you’re designing hardware today, that’s your product’s entire lifecycle.

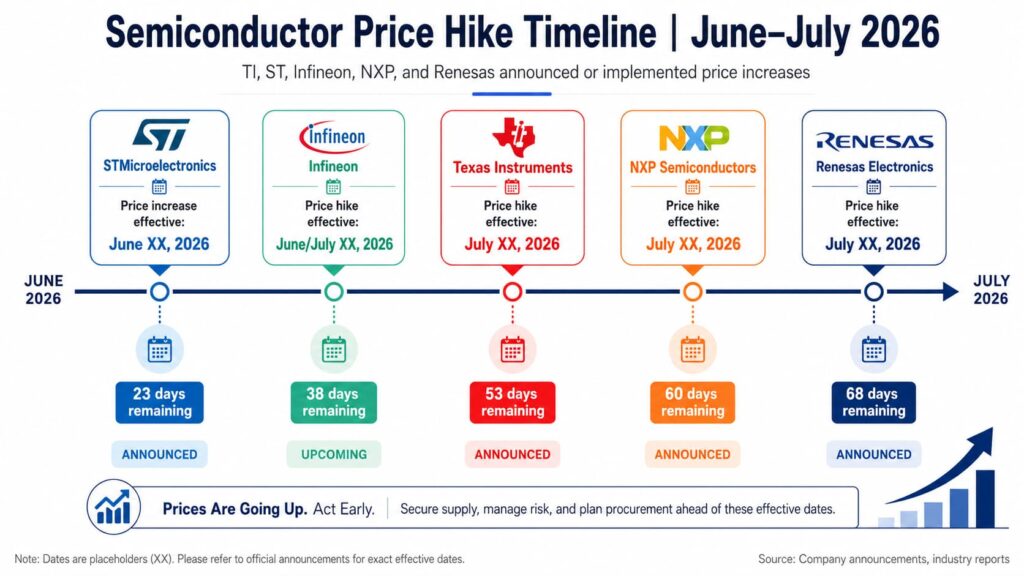

2. Who's Raising Prices — and How Much Time You Have Left

Here’s the situation as of today, June 22:

| Supplier | Round in 2026 | Effective Date | Products Affected | Time Remaining |

|---|---|---|---|---|

| NXP | 2nd | Jun 1 (in effect) | Full portfolio | Already active |

| STMicro | 2nd | Jun 28 | Products not covered in 1st round | 6 days |

| TI | 3rd | Jul 1 | Full portfolio | 9 days |

| Infineon | 2nd | Jul 1 | Power semiconductors (IGBT, MOSFET, SiC) | 9 days |

| Renesas | — | Jul 2026 | Selected product lines | ~2–3 weeks |

| Taiwan PMIC* | Following | Under negotiation | PMIC, DDR5 PMIC | TBD |

*Silergy, GMT, Anpec

Sources: AetrixElec, TrustCompo, ESMChina, ETime, Sina Finance

A few of these deserve more than a table row.

TI — three hikes in one year. I didn’t think I’d write that sentence. TI has always been the adult in the room on pricing. They’ve got the scale, the margins, the 300mm fabs. If TI raises prices, it’s usually because something structural has shifted — not opportunism, but genuine cost pressure. April 1 (15–85% on select products). May 7. Now July 1. If you’ve been treating TI as the stable-price anchor in your BOM — and honestly, who hasn’t? — that assumption is now a risk. “Finding a TI alternative” isn’t a strategic project anymore. It’s this quarter’s to-do list.

STMicro — six days. That’s not a typo. ST notified customers on May 28 and gave them one month. This round specifically targets parts that escaped the first adjustment on April 26. If you had line items that were untouched in Round 1, pull them up right now. They’re probably in scope this time. One month of notice for a second-round hike is… let’s call it aggressive.

Infineon — automotive power is in the crosshairs. They cited silicon wafer costs, specialty gases, energy, and maritime shipping in the notification. IGBT module backlogs already stretch into 2027. At this point, the price increase is functioning as a capacity allocation mechanism: pay more, or slip to the back of the queue. There’s no third option.

NXP has been running since June 1. Automotive MCUs (S32K3 series) and industrial processors are under simultaneous price and lead time pressure. Two problems for the price of one, as it were.

Renesas joining the synchronized repricing isn’t surprising, but it does mean five major suppliers are now in multi-round territory. That’s not coincidence. It’s a supply chain where everyone is looking at the same wafer allocation math and arriving at the same conclusion.

Taiwan PMIC suppliers — Silergy, GMT, Anpec — are the second wave. PMICs mostly live on 8-inch mature nodes, where utilization is pushing 90%. When TSMC and Vanguard reorganize capacity toward higher-margin advanced nodes, PMIC supply is the first casualty. Silergy’s AI ASIC Vcore PMIC is already sampling — which tells you where the high-end PMIC capacity is headed. Data centers, not your motor driver board.

3. Why Is This Happening? Three Forces, One Root Cause

Layer 1: AI structural demand. Everything else is downstream of this.

This is not a cyclical recovery story. HBM consumes 3–4× more wafer capacity than conventional DRAM, and all three producers are fully allocated through 2026. The chain reaction is straightforward: HBM eats wafer capacity → DRAM and NAND prices surge → mature-node capacity for PMICs, MOSFETs, and analog ICs gets squeezed → costs propagate everywhere.

TrendForce has already cut its 2026 server shipment growth forecast from 20% to 13%. The bottleneck isn’t demand — hyperscalers still want servers. The bottleneck is that the PMICs, BMCs, and voltage regulators those servers need have lead times stretching to 35–40 weeks. You can’t ship a server without power management.

Layer 2: Raw material costs. I’ve heard suppliers blame “input costs” for price hikes before, and sometimes it’s just a narrative. This time it’s real.

Copper above $10,000 per ton. Silver surging — which hits MLCC thick-film electrodes directly. Specialty gases, helium in particular, with Middle East shipping routes disrupted. Silicon wafer costs rising. Maritime freight rates climbing again. Infineon and ST both cited these factors explicitly in their hike notifications. When multiple suppliers point at the same cost inputs independently, the story checks out.

What’s unusual here is that these cost pressures are hitting simultaneously. Usually you get one or two at a time — copper goes up, or shipping gets expensive, or a fab has a fire. Right now it’s all of them at once, plus the AI demand wave on top. It’s a genuinely ugly combination.

Layer 3: Tariff-driven panic procurement — the self-fulfilling prophecy.

Accuris captured the moment precisely: semiconductor lead times spiked 67% in a single month (March 2026), jumping from roughly 25 weeks to 40 weeks. When buyers collectively rush to lock in orders ahead of tariff uncertainty, lead times don’t just lengthen — they spiral. The fear of shortage creates the shortage. We’ve seen this movie before — 2021, the automotive chip crisis — and the dynamics haven’t changed. What’s changed is that the underlying demand is structural this time, not a post-pandemic restocking bounce.

4. The MLCC Situation — Don't Sleep on This One

On June 17, TrendForce dropped a report that I think deserves more attention than it’s getting: high-end MLCCs for AI ASIC platforms are heading toward structural shortage.

The numbers are hard to ignore. During AMD MI450 platform validation, engineers replaced all aluminum electrolytic and tantalum capacitors with MLCCs. The result: 47µF 2.5V X6S 0402 MLCCs went from 1,440 pieces per board to 10,544 pieces — a 632% increase.

This isn’t just AMD being weird. NVIDIA Vera Rubin, Google TPU V8, AWS Trainium4, Meta MTIA — they’re all adopting similar high-density MLCC architectures. When every major AI ASIC platform converges on the same capacitor strategy, the aggregate demand spike is enormous.

Murata has started producing these specs but yields are under pressure. Their Izumo new fab won’t hit full capacity until 2027. Meanwhile, BB Ratios at major Japanese and Korean MLCC suppliers have been climbing month-over-month since April. High-capacitance X6S lead times have stretched from 8 weeks to 20 weeks.

Here’s what bothers me about this: the MLCC market has been through shortages before — 2018–2019 was brutal — but this time the demand driver is AI infrastructure, not smartphones. The volumes are larger, the specifications are more specialized, and the supplier base is narrower. There are only a few companies that can make 47µF 0402 X6S MLCCs at scale. If your procurement involves AI-related boards, Q3 strategic buffer stock for high-end MLCCs isn’t optional. It’s the difference between shipping and explaining to your customer why you can’t.

5. What to Do Right Now — No Theory, Just Moves

1. Lock what you can in the window you have.

ST’s June 28 deadline: 6 days. TI and Infineon July 1: 9 days. Pull every BOM line that touches these three suppliers. Which line items justify pre-buying? Distributors shorten quote validity after hike notifications — this is not the moment to deliberate. Act before the window closes. You can debate volume strategy after.

2. Start alternate source validation — yesterday.

Here’s a practical starting point, not a theoretical framework:

TI analog ICs (op-amps, LDOs, voltage references): MPS and Silergy have extensive pin-compatible alternatives. Richtek and SG Micro also worth checking. I’ve seen teams get surprised by how much overlap exists once they actually cross-reference.

Infineon MOSFETs/IGBTs: onsemi and ROHM are the obvious first stops. For SiC, look at ST and Wolfspeed. Don’t assume Infineon’s the only game in town — they’re the biggest, not the only.

ST MCUs: NXP and Renesas overlap in automotive and industrial. For non-safety-critical applications, GigaDevice and Artery have ARM Cortex-M alternatives that are pin-compatible enough to drop in without a board respin. Not always, but often enough to check.

NXP automotive MCUs: Renesas RH850 and TI Hercules (functional safety) are possible alternatives depending on the use case. Key word: depending. This is not one-size-fits-all.

Qualification takes time. If you start when the line stops, you’re already too late. The time to validate an alternate source is when you don’t urgently need it.

3. Abandon JIT for long-lead categories. I mean it.

PPSI‘s Q2 2026 language is blunt: “Relying solely on JIT manufacturing is a failing strategy in the current market.” They’re not wrong. For categories exceeding 40-week lead times — SiC MOSFETs, IGBT modules, automotive MCUs — build strategic safety stock. Place orders 4–6 months ahead. Yes, it ties up working capital. Running out of parts ties up the entire production line. Pick your poison.

Some teams I’ve talked to are doing this with a simple three-tier classification:

Strategic bottlenecks (custom ASICs, specific automotive ICs): long-term agreements plus dual-source where possible. Lock these in.

Leverage items (generic MOSFETs, standard analog): spot-buy aggressively, keep multiple suppliers quoting. Don’t get comfortable with one source.

Commodity items (resistors, standard caps): quarterly negotiation, safety stock at comfortable levels. These are boring — boring is good.

4. Verify per-part lead times. Category averages lie.

PPSI‘s supplier intelligence surfaced this: some approved Infineon MOSFET part numbers have actual lead times exceeding 52 weeks. The category average? 25–37 weeks. That gap isn’t a rounding error — it’s the difference between a production line running and a production line waiting. The average is a smoothing function that hides the specific parts that will break your schedule. Go line-by-line through your BOM. The parts with the worst lead times are usually not the ones you’d guess.

5. Don’t be a single-supplier hostage.

Remember Nexperia? When a single supplier hits trouble, the ripple effect moves fast. For strategic parts, maintain at least dual-source qualification — even if you don’t buy from the second source. Having a validated alternative gives you two things: negotiating leverage today, and insurance tomorrow. Both are worth the qualification cost.

One More Thing

Memory went from 29% to 53% of the global semiconductor market. That’s not a statistic. It’s a rearrangement of power.

When memory becomes the majority of the industry, wafer allocation follows. HBM gets priority because HBM carries the highest ASP. Mature-node analog and power ICs — the chips that actually go into motor drives, factory equipment, and cars — get squeezed to the margins. Not because they’re less important, but because they’re less profitable per wafer.

If you’re managing procurement right now, the question isn’t “when will prices come back down?” Goldman Sachs says 2028. Gartner says late 2027 at the earliest. Even the optimistic case gives you 18+ months of tight supply.

The question is: what does your supply chain look like after 18 months of this? Are you building resilience, or are you just chasing the next available reel?

Data sources: WSTS Spring 2026 Forecast, SIA April 2026 Sales Data, Goldman Sachs June 2026 Report, Gartner Q2 2026 Semiconductor Forecast, TrendForce (DRAM/NAND/MLCC reports), Accuris Technologies Lead Time Tracker, PPSI Q2 2026 Risk Report, Sourceability Q1 2026 Lead Time Report, AetrixElec, NAND Research, TrustCompo. All figures current as of June 22, 2026.

Alice lee

Business Manager

Focused on the electronic components sector, the author shares industry knowledge, product insights, and sourcing perspectives related to modern electronics manufacturing. With close attention to market trends, component applications, and supply chain developments, the content is designed to support engineers, buyers, and businesses in making more informed decisions.